It’s no secret that the COVID-19 pandemic was hard on the healthcare sector. From delays on routine medical procedures to the pressures the virus put on the first responders, the healthcare sector was impacted in a variety of ways – even some that investors may not have been truly aware of.

This includes hospital-backed municipal bonds.

But the COVID-19 crisis may finally be beginning to thaw for these municipal bonds and a new bull market could be starting. For investors looking at values in the muni sector, hospital and healthcare bonds could be a great bet.

Hit by COVID Crisis and Rising Rates

While the pandemic may be in the rearview mirror in terms of the virus, the outbreak is still having some wide-reaching effects. This is particularly true when it comes to hospital construction, expansion and funding.

Healthcare in the United States straddles the line between a public and private market. Because of this, the Federal government provides some tax benefits for serving the public. Bonds issued by hospitals are considered munis and their interest is free from Federal taxes. County and state-run hospitals and their bonds can be free of state/local taxes as well.

The problem is, unlike a state or local government, hospitals can’t tax their way out of default. As such, their muni bonds are based on revenues. Cash flow from operations goes to paying back their debt obligations. Revenue bonds are some of the most risky muni securities, and hospital/healthcare bonds are some of the riskiest of them all.

You can see these risks in action throughout the pandemic and into recent months with regards to rate hikes.

During the pandemic, hospital finances were strained due to new procedures and costs related to fighting the virus. For example, in California some hospital groups were paying nurses over $200 per hour during the shortage of staffing/worst of the pandemic. At the same time, many procedures – both elective and needed – were put on hold as fighting the spread of COVID became the priority.

The funding issues began to thaw in the post-COVID years. However, the surge in interest has started to hurt as well. Now, many healthcare groups are facing very steep borrowing costs as their cash reserves are running thin.

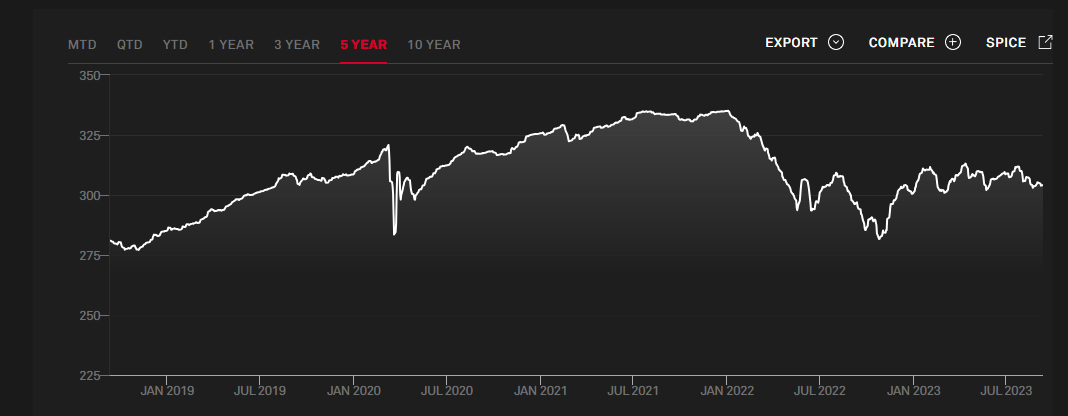

This chart of the S&P Municipal Bond Hospital Index shows the two big dips due to COVID and rate hikes.

Source: S&P Dow Jones Indices

A New Bull Market for Hospital Revenue Bonds

However, municipal bond investors may not want to throw away these hospital bonds just yet. According to fixed income specialist Lord Abbett, they may actually be a bargain in the making and a new bull market could just be starting.

For starters, Lord Abbett suggests that the recent downgrades to hospital bonds were backward-looking, not forward-looking. Many of the credit and cash flow issues are starting to wane. The fixed income manager cites a Kaufman Hall survey of 900 leading hospitals and healthcare groups showing that the average hospital operating margin improved every month during 2022. These margins finally turned positive in December of last year and are showing profits or strong operating cash flow at the average hospital. Moreover, the Kaufman survey shows that median contract labor rates have declined, from $200 per hour down to just $126 by the end of the year. They have further dipped in 2023. 1

At the same time, procedures and billable numbers have continued to trend higher. Consumers have once again returned to spending on healthcare, while the strong labor market has allowed more people to participate in the healthcare system via employer healthcare plans. The added benefit for hospitals is that many procedures are now being done via outpatient facilities, while telemedicine and walk-in clinics are being used for first points of contact. These options all come with higher margins for the hospital groups and potentially allow for additional billable services later on.

The end result to Lord Abbett is that many hospital groups may not be on as shaky footing as their recent price declines would have you believe. The surge in margins could make these bonds and their high yields a top draw for investors.

Adding Some Hospital Muni Bonds

Given their high tax-free yields and potential, investors may want to consider adding hospital revenue bonds to their portfolios. However, there are caveats to consider when looking at the sector.

For starters, like most muni bonds, it can be difficult to get your hands on individual issues. Thanks to the fact that bonds trade over the counter, investors may be forced to pay big premiums to buy them, or worse, find no buyers if they wish to sell them.

Secondly, because their only source of repayment is revenues, hospital bonds are riskier than general obligation bonds issued by states or local governments. As such, they are considered high-yield muni bonds. Some of them may carry alternative minimum tax (AMT) exposure. While the vast bulk of people are immune to the AMT, some taxpayers still get caught-up in the secondary tax system. Hospital muni bonds could be an issue for those taxpayers.

So how to buy them? Going broad is best. There is no direct hospital bond ETF or fund…yet. But they do feature prominently in many high-yield muni funds. The indexed-based SPDR Nuveen Bloomberg High Yield Municipal Bond ETF has about 17% of its holdings in healthcare muni bonds, while the VanEck High Yield Muni ETF has about 12%.

Another option could be to go active. Active managers don’t have to follow what an index holds and can load up on bonds they feel are trading at discounts, including hospital munis. But investors need to check holdings data. Some managers like the BlackRock High Yield Muni Income Bond ETF have less than 5% of their assets in hospital bonds. A good choice could be the Lord Abbett High Yield Municipal Bond.

Muni ETFs & Mutual Funds With Exposure to Hospitals

These funds, with an exposure to hospital bonds, are selected based on year-to-date total returns. Their expense ratios range between 0.32% to 0.85%. They are yielding between 4% to 5.5% and have AUM between $60mn to $8.5bn.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| PHMIX | PIMCO High Yield Municipal Bond Fund Institutional Class | $2.95B | 3.4% | 5% | 0.57% | MF | Yes |

| HYMAX | Lord Abbett High Income Municipal Bond Fund Class A | $3.45B | 3% | 4.2% | 0.75% | MF | Yes |

| HYMU | BlackRock High Yield Muni Income Bond ETF | $60.6M | 2.9% | 4.7% | 0.34% | ETF | Yes |

| HYMB | SPDR Nuveen Bloomberg High Yield Municipal Bd ETF | $1.95B | 2.8% | 4.3% | 0.35% | ETF | No |

| ORNAX | Invesco Rochester Municipal Opportunities Fund Class A | $8.41B | 2.6% | 5.2% | 0.85% | MF | Yes |

| HYD | VanEck High Yield Muni ETF | $2.92B | 2.3% | 4.3% | 0.32% | ETF | No |

No matter how investors choose to purchase their exposure – either through funds or individually – hospital revenue bonds could be an interesting high-yield play for their income portfolios. While they are risky and have had hard times, the current trends showcase a bullish future. One that supports their cash flow and high tax-free yields.

The Bottom Line

The pandemic and the rising rate environment hit hospital bonds right in the wallet. However, the freeze is starting to thaw, with these bonds offering plenty of high yields and tax benefits. For risk-seeking fixed income investors, buying these muni bonds makes sense.

1 Lord Abbett (June 2023). Municipal Bonds: Bullish Signs for the Hospital Sector